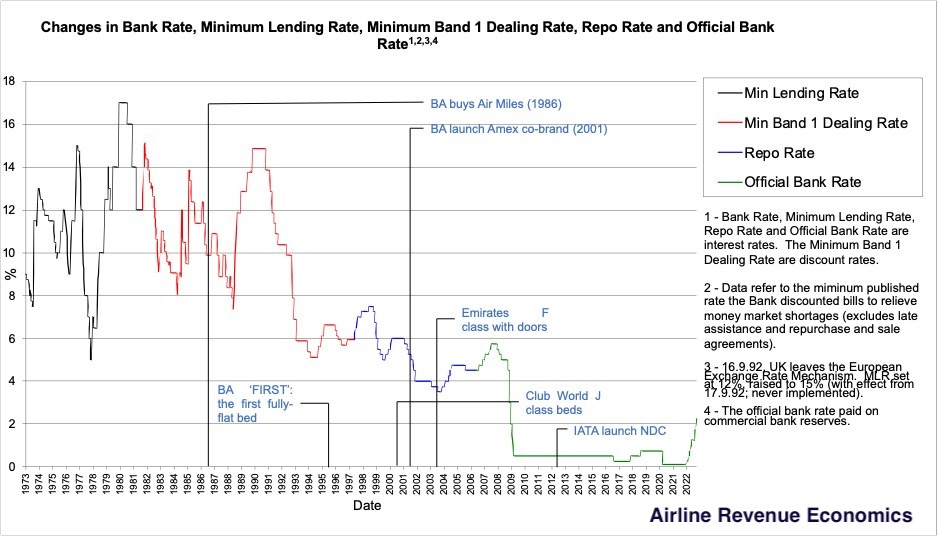

Show me the Monetary Policy

Rising interest rates might render One Order & One ID irrelevant, but other technologies could do well

Economic theory is cleft in two. Macroeconomics studies growth, innovation, employment and money. It studies regions and nations over centuries. Micro tries to understand how individual families and firms decide what to do every day.

Modern macro theorists sanity check their ideas by figuring out whether or not they are consistent with micro theory. Cons…